Level 3 data: A portfolio manager’s key to liquidity risk measure in times of uncertainty

Author: Masami Johnstone, Senior Client Advisor, BMLL

First published in Traders Magazine, February 2023

Amid challenging and volatile markets and negative stock performance in 2022, how can portfolio managers control portfolio liquidity risk effectively and maximise the returns from these investment decisions? Masami Johnstone, Senior Client Advisor at BMLL, argues that a data-driven dialogue between the investment team and trading desks is imperative to measure portfolio liquidity risk and support the investment decision-making process.

In general, most stock markets ended the year 2022 with a disappointing performance.

2022 was a challenging year for stock markets. Stock performance was negatively affected by the uncertainties resulting from the Russia and Ukraine conflict, the spike in inflation and the subsequent cost of living crisis. Additionally, China's battle with COVID-19 continues to put significant pressure on global supply chains.

Major US indices fell significantly during the year, with Dow falling -9%, S&P 500 -20% and Nasdaq Composite Index -34%. In Europe, the STOXX 600 recorded a fall of -13% in 2022. Amid this grim picture, the resilience of FTSE100 was remarkable to end the year with a +1.2% flat performance*. The general downturn in equities led the investment community to hunt for safe havens to prepare for further economic downturns and the looming recession. These assets included UK-based stocks, for example, AstraZeneca (Healthcare) and Unilever (Consumer Defensive). These defensive favourites achieved positive performance during the year, up 32% and 5%, respectively.

In this article I’ll examine the typical characteristics of these defensive stocks during 2022. Did they have favourable trading conditions? And most importantly, how can portfolio managers control portfolio liquidity risk effectively and maximise the returns from these investment decisions? Leveraging the most granular venue data provided by BMLL, this article explores potential new liquidity risk measures for the investment community.

Non-Addressable liquidity: a new liquidity risk measure?

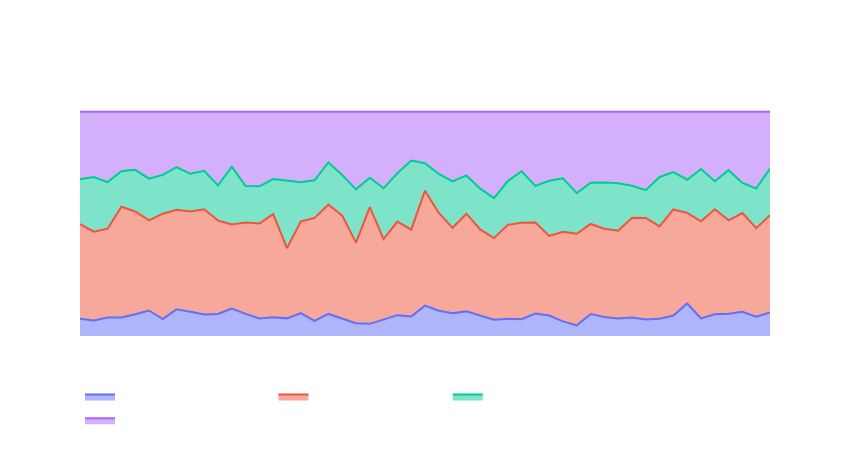

Let’s take a closer look at the liquidity classification breakdown for AstraZeneca and Unilever in 2022 - Exhibit 1a and 1b. Harmonised cross-venue data categorises trade liquidity for each stock into four categories; Lit, Non-Addressable, Bilateral (Bi) and Dark. Not surprisingly, Lit Exchanges provided the most liquidity for both names - 42% of the total notional for AstraZeneca and 37% for Unilever were executed on Lit Exchanges on average in 2022. However, most participants are unaware that the second largest group by volume was Non-Addressable liquidity. For AstraZeneca, Non-addressable liquidity accounted for 30% of the total liquidity on average, while Unilever's Non-Addressable claimed 36% of total liquidity.

Exhibit 1: AstraZeneca and Unilever - Liquidity Classification (Weekly Average).

So what does this mean for portfolio management risk? Non-Addressable liquidity includes various OTC trades, such as trades in a different currency to the primary currency the security is traded in, out-of-hours trades (off-book), trades tagged as non-price forming or trades executed at off-market prices. However, these trades are not available for general market participants. In AstraZeneca and Unilever's case, this means that only 70% and 64% of the published volume was available for institutional investors on average during 2022.

Portfolio managers who place large institutional orders must know the potential risk associated with Non-Addressable liquidity. Ignoring this can inadvertently lead to higher liquidity risk for the portfolio.

Looking at Auction Dislocation to improve trading and portfolio performance

Another metric that allows portfolio managers to control portfolio liquidity risk effectively and maximise the returns from these investment decisions is to consider auction dislocation. This is particularly important when orders are placed to the target closing price of the day. Closing auctions typically account for more than 20% of the total volume on Lit exchanges. However, there is no guarantee that large institutional orders can be executed at a desirable price or fully filled at the closing auction session.

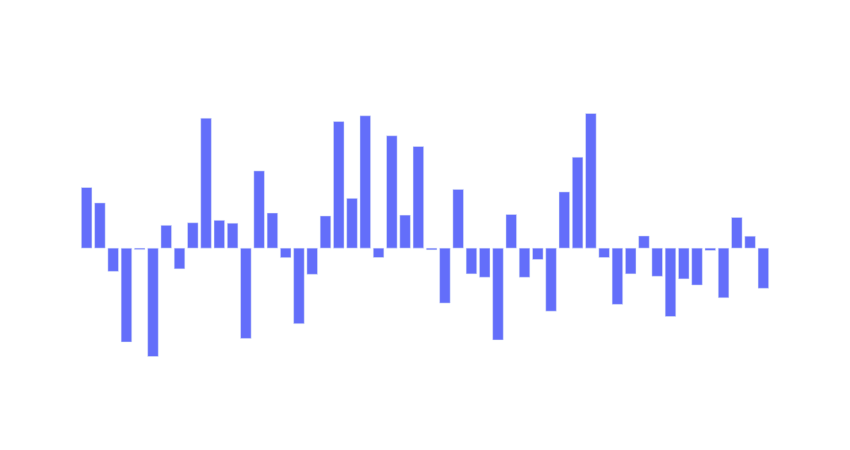

Let's look at the historical price behaviour of AstraZeneca and Unilever at the closing auction. Exhibit 2a and 2b indicates the price dislocation at the closing auction using BMLL Level 3 Data. One of the metrics it captures is the last price at the continuous trading session, i.e. the last tick price before the closing auction starts. Exhibit 2 compares the "pre-auction" tick price and the day's closing price to gauge the level of price fluctuation for AstraZeneca and Unilever.

Exhibit 2: Auction Price Dislocation (bps) for AstraZeneca and Unilever (Weekly Average) **

Throughout 2022, closing prices for AstraZeneca and Unilever fluctuated compared to the pre-auction prices. This means that execution prices can be considerably away from the prevailing price level before the closing auction starts.

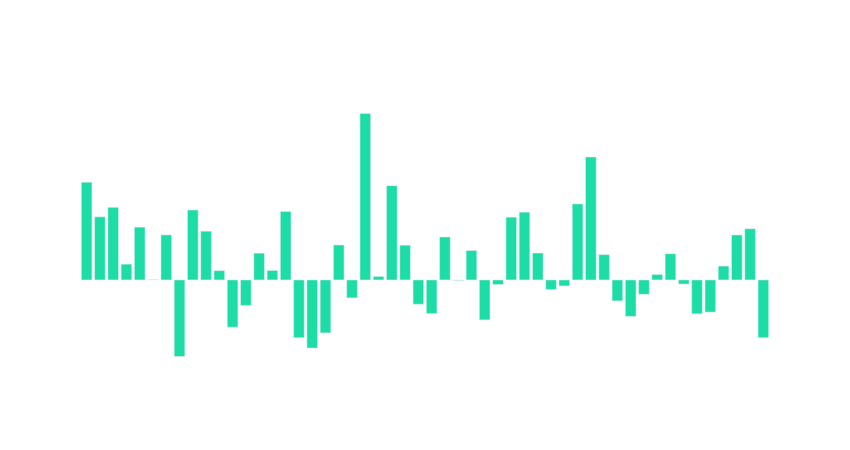

Additionally, there is no guarantee that large orders can be fully matched at the closing auction. Exhibit 3 indicates the notional value of the daily "outstanding" orders after the closing auction. The metrics show the excess notional volume after the closing auction that stays on the book. The value is expressed as the notional volume of bid orders at the crossing price minus the notional volume of ask orders at the crossing price.

Exhibit 3: Auction Order Imbalance for AstraZeneca and Unilever – Notional (Weekly Average) **

As we can see, significant volumes were often unmatched at the closing auction, and they remained on the order book after the auction ended.

A complete picture of market conditions, such as auction dislocation and order imbalance, can only be captured if market participants have access to the full order book, including Level 3 data. Level 3 metrics can provide portfolio managers and traders with vital information for portfolio liquidity risk, as explained above.

A data-driven dialogue between the investment team and trading desks is imperative

My article in June 2021 explored the importance of enhancing execution analytics using granular venue data. Since then, the trading community has started to use such data sets for more in-depth execution analysis to better understand complex order interaction behaviour across multiple venues and trading mechanisms, increasing the chance of achieving best execution.

So what is next? During this time of uncertainty, it is important that a strong dialogue between investment teams and trading desks exists, to best prepare market participants for unexpected events during executions. In particular, it is crucial to have data-driven discussions supported by the common knowledge of in-depth market dynamics. The metrics such as Non-Addressable liquidity, auction dislocation and auction order imbalance can be used as key measures for portfolio liquidity risk to support the investment decision-making process. This will ensure trading desks can anticipate the challenges they may face to secure liquidity during executions.

Over the years, the industry worked hard to improve the dialogue between portfolio managers and traders, especially around liquidity discovery. I believe by using untapped insights from the most granular Level 3 data participants can progress in this journey further.

Note: Insights are based on BMLL Level 3 Data, which helps trading desks understand complex market behaviours across venues and trading mechanisms. BMLL has developed comprehensive trade classification metrics, which the trading community now actively uses to monitor the quality of executions.

Notes:

* Index performance between 1 January - 31 December, 2022.

** Source: BMLL Level 3 Data